.jpeg)

.jpeg)

.jpeg)

Also known as “ Construction Loan” or “Progress Payments Loan”. You buy the land at the very beginning of the build, then have a construction contract with the builder to build the house on the land. However, you (or the lender) make progress payments to the builder at certain stages of the construction (i.e., when the foundations have been completed, when the framing is up, when the roof is on etc.). until the house is completed (with CCC issued). You start to pay interest on your loan as soon as the land settled and your mortgage payments increase at each stage as you pay interest on any funds released by the lender.

The construction loans are exempt from the Reserve Bank of NZ restrictions. This means you can potentially build a new home with 20% deposit if it is an investment property and with as little as a 10% deposit for first home buyers. Certain conditions apply and we are happy to help with it.

.jpeg)

.jpeg)

A fixed-price contract where the developer/ builder takes all the cost upfront and you pay the deposit (usually 10%) to indicate your interest in purchasing and pay all the rest of the money once the house has fully completed (CCC issued). You do not have to make mortgage payments until the property has been completed and settled.

This contract is exempt from the Reserve Bank of NZ restrictions. This means a 10% deposit for first home buys (20% deposit for investment properties) is required for a turn-key contract.

This contract is exempt from the Reserve Bank of NZ restrictions. This means a 10% deposit for first home buys (20% deposit for investment properties) is required for a turn-key contract.

- Buying off the plan means buying a property that hasn't been built yet or is still under construction. You make your decision to buy based on the building plans and designs, rather than the finished product.

- Pros and cons of buying an Off-plan property:

- One main advantage of buying property off-plan is the ability to secure the purchase at below market value.

- Small deposit and staged payments.

- An extended settlement period gives you more time to get your finance sorted.

- The risk in buying off-plan is that you are legally bound to complete that purchase once the developer delivers the project – so your deposit and your mortgage approval are tied up should you decide you want to exit the contract.

- Thinking of buying off-plan? Talk to us first.

.jpeg)

.jpeg)

- If you are not relatively experienced in the construction industry (ie., site management, hiring, managing and paying all contractors, buying materials, health and safety on the building sites and being familiar with building codes), we would not recommend you to bind in this type of contacts.

It is a programme from the NZ government that aims to build affordable homes for eligible first home buyers.

Who is eligible?

- A first home buyer ( or a “second chancer” in a similar financial position to a first home buyer).

- A New Zealand citizen or permanent resident.

- The total income before tax must be no more than $120,000 for a single buyer and no more than $180,000 for more than one buyer.

- Must intend to live in the property as your main home for at least 3 years. The Government is amending this rule so that studios or single bedroom properties that are purchased are only required to be owned for one year.

- *second chancers are people who have owned a home before but do not have any more. All second chancer must meet an asset cap (an asset cap is anything that can be used or sold to put towards a deposit e.g. cars, savings or stuff. KiwiSaver funds is excluded). A second-Chancer’s assets must be less than $80,000 to $120,000 depending on where they reside in New Zealand.

- You must enter a ballot for any or all of the available properties that you are interested in purchasing. If successful at any ballot, you can only purchase one property. Getting a pre-approved home loan or mortgage can certainly speed up the process of getting full loan approval once you’ve found the property to buy. That’s where our adviser can help.

.jpeg)

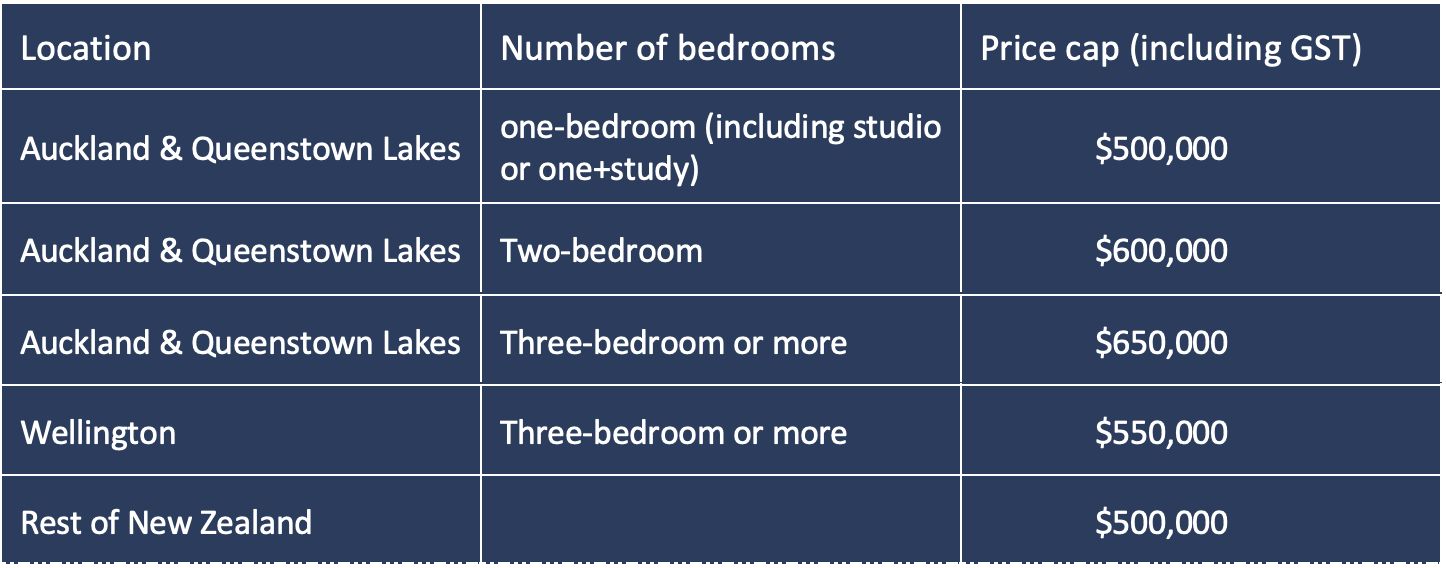

- How much will a KiwiBuild home cost?

Talk to an adviser

Need a professional mortgage adviser?