.jpeg)

What will we do for you?

- Calculate affordability

- Nail your deposit

- Help you arrange the property inspection and valuation

- Negotiate a great deal from the bank and get the best loan structure

- Help to get KiwiBuild pre-approval

- Help to get up to 95% LVR (strong financial situation)

.jpeg)

.jpeg)

what do you need to know before buying your first home?

.jpeg)

Gifted by a close family member

The deposit has already been paid towards the property

As a first home buyer, you can withdraw your KiwiSaver contribution as part of a deposit towards your new home. If you:

- have been a KiwiSaver scheme member for at least three years;

- You're going to live in the home you're buying or build a home to live in on the land you're buying.

- It's the first time you've made a KiwiSaver withdrawal to buy a home.

- After you use KiwiSaver funds to buy your first home, you must leave at least $1000 in your KiwiSaver account.

Want to know more about KiwiSaver?

have more questions about the first home grant?

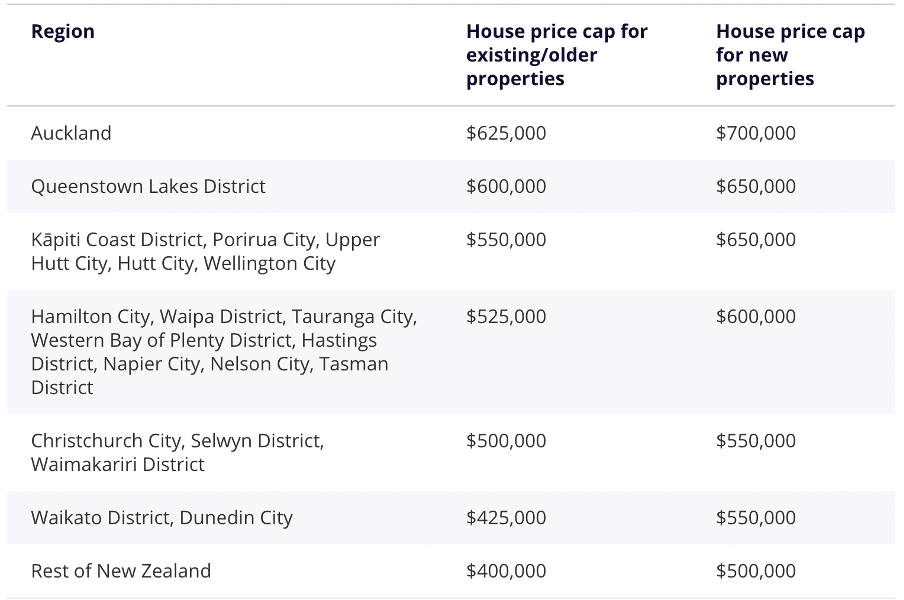

In addition to KiwiSaver, the First Home Grant provides eligible first-home buyers with an extra boost of deposit. Eligible criteria are as follows:

- you earn $95,000 for a single buyer or your household income is less than $150,000.

- you are buying an existing/older property for less than $625,000 in Auckland, $600,000 in Queenstown (Lake District), $500,000-$550,000 in other metropolitan areas or $400,000 in rural New Zealand.

- you may be eligible for a First Home Grant of up to $5,000 for five years per buyer.

- You can combine this grant with an eligible partner for up to $10,000.

- If you are purchasing (or build) a brand new property less than $700,000 in Auckland, $650,000 in Queenstown (Lake District), $550,000-$650,000 in other metropolitan areas or $500,000 in rural New Zealand.

- you may be eligible for a First Home Grant of up to $10,000 for five years per buyer.

- You can combine this grant with an eligible partner for up to $20,000.

Fixed Interest Rate Loan

Where you fix or lock the interest rate for a period of six months to five years. At the end of the term, your loan reverts to a floating rate or you can choose to fix the rate again for a new term or change to a different loan structure.

Advantages:

- You know exactly how much each repayment will be over the term.

- Lenders often offer competitive specials fixed rates.

- You can lock in lower rates if market interest rates are rising.

Disadvantages:

- Can be more difficult to make extra repayments.

- If you take a long term, there is a risk floating rates may drop below your fixed rate.

- If you choose to sell your property and/or break a fixed loan you may be charged a ‘break fee’ to terminate early.

.jpeg)

.jpeg)

Floating/ variable interest rate loan

Where your interest rate can increase or decrease as interest rates in the market change, normally linked to the Official Cash Rate (OCR).

advantages:

- You have more flexibility to make changes without penalty, such as paying off the loan early, make a lump sum payment, extra payments or changing the loan term.

- You can refinance the loan at any time without penalty.

- If interest rates drop your loan repayments will reduce.

disadvantages:

- If interest rates rise, your mortgage repayments will increase as well.

- The interest rate may be higher than a fixed-rate mortgage.

Mixed fixed and floating interest rate loan

You can split a loan between fixed and floating rates.

Advantages:

- This lets you make extra repayments without charge on the floating rate portion.

- You have certainty over the fixed portion of the loan.

- Splitting a loan can give you a balance between the certainty of a fixed rate and the flexibility of a floating rate. It gives you a mix of interest rates so any rises and falls will not cause big changes in your repayments.

Disadvantages:

- Rising interest rates will affect the floating portion of your loan.

- How much of your loan you have in each portion depends on which of these is more important to you.

.jpeg)

.jpeg)

Off-set loan

An offset mortgage setup can reduce the amount of interest you pay on your mortgage. Typically, interest is payable on the full amount of a loan. But by linking your loan to any savings or everyday accounts you already have, you pay interest on that much less. For example, someone with a $500,000 mortgage and $40,000 in savings would only pay interest on $460,000.

The more cash you keep across your accounts from day to day, the more you’ll save because interest is calculated daily. Linking as many accounts as possible – whether from a partner, parents, or other family members – means even less interest to pay. However, the linked savings accounts do not earn any interest when they offset a loan. Best for those who have uneven income and are very good at controlling their finances.

Table loan

Known as a Principal and Interest (P&I) loan. This is the most common type of home loan. You can choose a term up to 30 years with most lenders. Most of the early repayments pay off the interest, while most of the later payments pay off the principal (the initial amount you borrowed).

Revolving credit

A loan account is similar to a giant overdraft, as all your income and expenses come out of the one account and you can redraw up to the limit at any time. Some revolving credit mortgages gradually reduce the credit limit to help you pay off the mortgage. By keeping the loan as low as possible at any time, you pay less interest because lenders calculate interest daily.

Reducing loan

Also called straight-line mortgages. You pay the same amount of principal with each repayment, but a reducing amount of interest each time. These are quite rare in New Zealand. If you can manage higher payments, it would be better to take a table loan with extra or high payments for the whole term, in order to pay less interest.

Interest-Only loan

When you only pay interest and no principal. Some borrowers take an interest-only loan for no more than 5 years and then switch to a table loan. Ultimately it costs more as you will still owe the full amount that you borrowed until the interest-only period ends and start paying back the principals. These loans are often used for property investment.

Repayment Frequency

Loan payments can be made weekly, fortnightly, or monthly (if you paying I/O). Paying more frequently can result in slightly lower interest costs during the lifetime of mortgages.

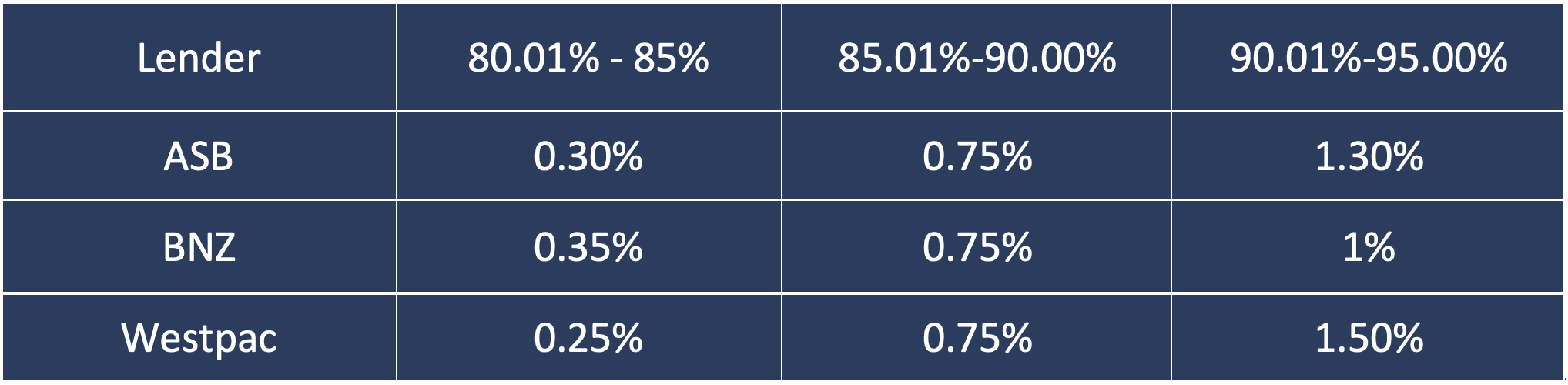

Low equity margin

A low equity margin (LEM) s is basically a higher interest rate charged on your home loan because the banks see lending of more than 80% as a higher risk and there are additional funding costs to the banks. The banks charge a higher interest rate to cover the extra risk and to offset the higher bank funding costs associated with lending with low deposits. The banks generally scale the margin charged depending on the LVR (loan-to-value ratio) on your home loan.

.jpeg)

Low equity premium/ fees or margin

A low equity fee is a one-off charge, which can be added to your home loan amount, so you don’t have to pay it upfront.